The super non-obvious guide to raising a Series B

10 non-obvious rules for founders and VCs

SafeGraph recently raised a $45M Series B and I have gotten a ton of inbound from entrepreneurs in similar stages for best practices. This piece is for other entrepreneurs but also for venture capitalists who want to better understand what crazy founders are thinking. This was originally published on the SafeGraph blog.

If there is one thing common across humanity, we all just want to be loved and felt loved.

If you are looking for a spouse, my best advice is your number one criteria for a partner should be someone that truly loves you. And if you are picking a venture capitalist to be your financial partner, find the firm that most loves your business.

So, without further ado, here are the ten non-obvious rules to raising a Series B -- both for founders and VCs...

1. Get Ready to Work REALLY Hard … Because It Will Be Hard

SafeGraph raised $45 million with a $370 million valuation. We started pitching firms on Jan 5 and we selected a term sheet on Feb 11.

We had a great outcome but we need to remember that this is probably the best time in history to raise money. Anyone that tells you that raising money is easy is either completely high or lying. It was a crazy amount of work and super intense. Prior to the fundraise, we spent HUNDREDS of hours getting ready. It took two months of intense work to get ready to start fundraising. And during the fundraise (an intense six weeks) I was often doing 7 meetings a day and it was completely consuming.

2. Don’t Let the Fundraise Slow Down the Business -- That’s Your Priority as CEO

Unfortunately, I’ve seen a lot of CEOs use fundraising as another opportunity to delegate work to other employees. If there is ever a time NOT to do that, it is during a fundraising. One of your main priorities during a fundraise should be to make sure your business doesn’t slow down during this time, and for that to be true you’re going to need to do a lot of the work yourself.

You should pick a small number of people internally (three max!) to help you jump headfirst into the fundraising effort. Ideally these folks are not from teams responsible for important growth initiatives, like product, sales, or marketing. In my case, I was able to rely heavily on our VP of Operations, VP of Finance, and my executive assistant. Although this created significantly more work for the three of us, it allowed the rest of the organization to stay 100% focused on growing the business.

As you’ll soon find out, the fundraising process can be a long and drawn out process. This is precious time that shouldn’t pull a bunch of key employees away from their main priorities. One advantage here is that if you can accelerate the business during this time, you can use it to get better terms and have more leverage to push for a fast close (more on that later).

I did send out a weekly detailed update (with a full funnel analysis) to the SafeGraph Executive Team and to our board of directors. That kept them in the loop and also helped them keep me accountable for my goals.

Maybe surprisingly, a way to measure how well a fundraising went is by how few people internally were involved (or even knew about it!).

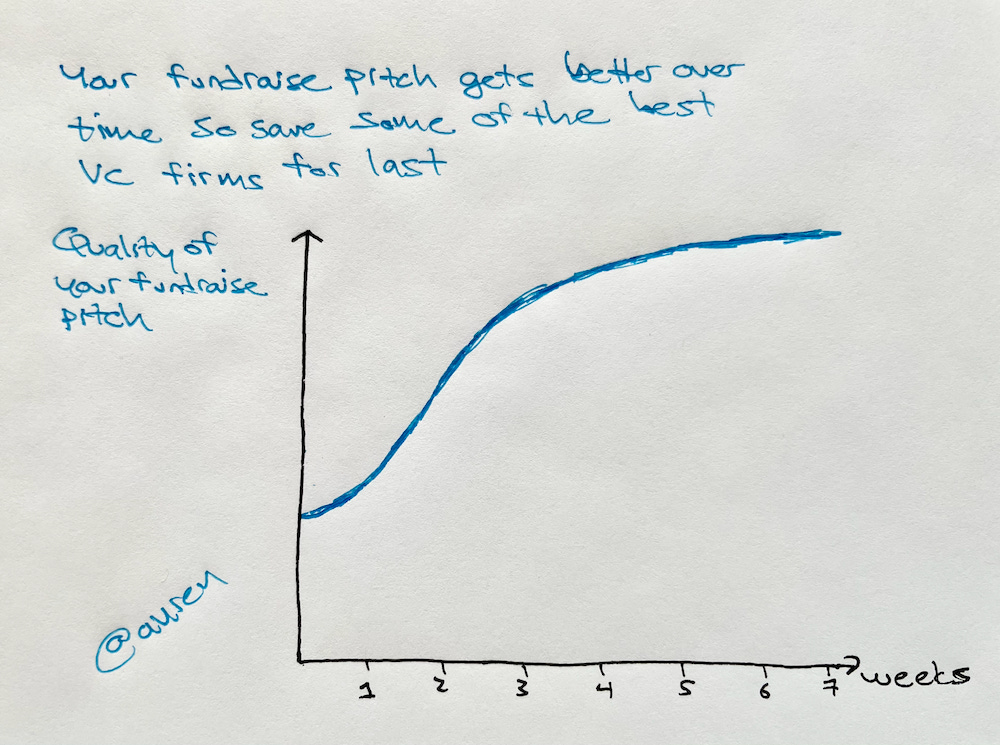

3. Your Pitch Gets Better Over Time -- So Pitch Some of the Best Firms Last

None of the firms we talked with in the first 3 weeks of pitching gave us term sheets … and most passed after just one or two meetings.

In contrast, we got four term sheets from firms we pitched in the following three weeks and over a dozen of those firms went into deep due diligence (and many ultimately dropped out because they could not move fast enough due to a compressed timeline).

Our pitch in week 4 was markedly better than in week 1. Luckily, many of the VCs we most wanted to talk to were later in the process (including Sapphire, our eventual partner, which was one of the top three firms we were hoping for) … but I flubbed meetings with many storied VCs early until I had my pitch down.

Your first full pitch shouldn’t even be with a VC. I did over 8 practice runs before pitching VCs but, in retrospect, I should have done more.Special thank you to Tod Sacerdoti, Alex Rosen, Brendan Baker, Travis May, Jeff Lu, Ravi Patel, Nicole Berger, Ross Epstein, and many others for their incredible help.

4. ALWAYS Do What You Say You Are Going to Do

If you tell a VC you will give them access to the data room by the end of the day, then give them access to the data room by the end of the day. If the data room is not ready, tell the VC it isn’t ready and let them know when they will get it.

We were really good about setting expectations to the VCs. In a few cases we promised a document (like a deeper dive) and forgot to send it and that eroded trust.

And trust is two-ways. For VCs: if you tell a CEO you will get back to her by Monday night, then you should get back to her by Monday night. Don’t wait until Tuesday to get back to her. You lose credibility everytime you don’t do what you say you will do.

During our process, a few VCs promised “we will review the materials and get you our thoughts on next steps by Thursday” and then Thursday came and went without hearing from them. I would hear from them a few days later (“sorry about that, something came up. We are super interested -- can we set up a meeting with my partners?”). Great VCs prioritize managing their time better … they just send an email before the deadline letting the founders know a few more days are needed.

Great companies have no desire to have someone on their board that cannot keep their promise (or manage themselves). Board members are expected to do a lot of work and companies want a VC to prove they are going to be a good member during the process.

Luckily, most VCs were very good at keeping their promises and being on top of things. I found a VC’s responsiveness was extremely correlated with the reputation of the firm. VCs with very high reputations (like Sapphire) were extremely responsive (even with a quick “no”). VCs that are considered third-tier were much less likely to be on top of things. I came into the process thinking it would be the opposite -- that third-tier VCs would work harder because they need to build their reputation … but it turns out that high-reputation VCs have high reputations for a good reason.

5. Never Ever Be Oversubscribed

Too many of my entrepreneur friends have over-subscribed rounds. They have eight different options at the same price and they are taking the time to pick between those options. This makes no sense.

They even brag that they are oversubscribed.

Bragging that you are oversubscribed is like bragging about the “pop” on your IPO -- it means you have under-optimized the round and left money on the table (and hurt your existing shareholders).

If you are truly oversubscribed, that means you had way more demand than supply and you could adjust your price. One company I am an angel investor in recently raised $40M in new money and said they were oversubscribed by $300M. That certainly means they could have gotten a much better deal.

The demand in your company should be reflected in the price. If you find yourself having to cut back lots of people or cutting back on allocation, then you should have the power to change the terms and make them more favorable to current shareholders.

Lots of VCs (famously, Bill Gurley at Benchmark) complain that companies under-optimize their IPOs and that complaint rings true. But companies seem to massively under-optimize every financing round … not just the public financing.

6. Minimize the Time Between Term Sheet and Close

Usually when a company signs a term sheet, they also sign an exclusive for 30 days. It is in both sides’ best interest to close much faster than 30 days, but most VCs do not realize this. Most VCs, even ones that run a great deal process, completely delegate the close process to their lawyers.

That is a mistake.

The time between term sheet and close is precious.

In addition, the closer the time gets to 30 days, the LESS leverage the VC has. VCs should try to close in 10 days and push the company to move faster. Instead, in almost every deal, the company is pushing the VC to move faster.

As you get closer and closer to the 30 day mark, the exclusivity is closer and closer to expiring. Once the exclusivity expires, the company can pick up its head and re-engage all those other investors that put in term sheets … and can engage them with docs that are likely 99.9% done. So the company has all the leverage.

In addition, now-a-days companies are growing so fast that they usually grow significantly in 30 days -- so they are ACTUALLY worth more if you apply the same multiple logic.

I was once involved in a merger transaction that was worth hundreds of millions of dollars. The acquiring company decided to renegotiate the deal at the very end of the process to save them $5 million (which was less than 2% of the deal at the time). The problem was, the acquiring company decided to negotiate in the 11th hour, exactly when their leverage was disappearing. They seemed to think they had MORE leverage at the end of the exclusivity period for some reason. Because of this, the 30-day window lapsed and the target company had the ability to shop for more offers. In the end, the deal closed a week later at a 30% HIGHER price … the acquiring company tried to save 2% but ended up losing 30%. Lesson is to always understand when you have leverage and when you don’t.

The closer the deal comes to the 30-day mark, the more risk the VC takes that a company might shop the VC deal. I know that does not happen much, but in today’s hot market, it is not a risk a VC should take. Smart VCs should try to get the entire deal closed in 10 days (and it is very possible to do that), not 30.

7. VCs Should Not Optimize For Small Terms

There are just three main drivers that affect VC returns: (1) the company they invest in, (2) the price, and (3) the amount they invest. I’d wager that those three factors alone account for over 98% of the returns of a fund.

So everything else that is worked on between term sheet and close (the docs can number many hundreds of pages and take a hundreds of collective hours to draft and negotiate) make up less than 2% of all returns a VC might get (see great Twitter thread by Villi Iltchev and another by Jamie Goldstein).

Everything between term sheet and close is about protecting a VC’s downside … but the power-law returns of most VC firms show that downside protection is a very small driver of overall return.

And while 2% is not insignificant, the time it takes for the VC prevents them from spending more time helping their portfolio companies, and also makes them spend less time looking for new deals. In addition, the closing process takes a LOT of time of the CEO and other key employees of the company -- time which could be better spent making the company better.

There is usually an extra $50k in legal fees (sometimes a LOT more) that is needlessly spent just to negotiate downside protections on extremely low-probability events.

VCs would make almost an identical return just investing in common shares (which is what public markets investors do). The big reason not to invest in common is that it hurts a company’s 409a valuation and thus means option pricing would be higher.

A smart VC would advertise super vanilla Series B docs. They would not have any of the stuff that takes all the time of close. This would:

Allow the Smart VC to win more deals

Enable deals to close much faster (most deals today take at least 30 days from term sheet to close)

Allow the smart VC to spend more time helping their portfolio companies and searching for new deals

Immediately put the smart VC and the founders on the same team (and reduce the adversarial time between term sheet and close).

Of course, this only makes sense for VCs that make power-law returns. It likely does not make sense for traditional private equity firms.

8. VCs Should Not Use GLG for Customer Calls

A LOT of the VCs we engaged with spun up customer calls through GLG. In theory, that’s fine. In practice, it makes less sense.

For GLG, it is REALLY hard to find a user of a product at a large company. Let’s say your customers are Pepsi, Starbucks, American Express, Walmart, Amazon, and a few random start-ups. You can be sure that everyone GLG introduces you to will be at those few random start-ups and none of them will be at the big companies. At a start-up of 30 people, it is really easy to find the person that uses a company’s product. At a huge company with 10,000 employees, it is virtually impossible to find the right person.

So most VCs spend their time doing customer references of the company’s least valuable customers.

Moreover, MANY of the people the VCs talk with are actually just posing as customers (they are people tangentially related to the company) because these “experts” just want the quick money from the call. So then the VCs just get random data.

In SafeGraph’s case, one well-known VC shared the four calls they did with SafeGraph “customers” through GLG. Two happened to be our two smallest customers. And two were random guys who were tangentially related to our market but definitely not customers. This was a waste of time for the VC and gave them a false impression of SafeGraph.

9. Bad News By Email, Good News Also By Email

I MUCH prefer bad news via email. If a VC passes on a company, they should send a quick email “we really like the company but we are passing. Want to set up a call tomorrow so we can walk through our reasons?”

Instead, many VCs send a cryptic email to the CEO -- “you free for a quick call tomorrow?” The founder then moves around three other meetings to make time only to get a pass.

Not only should VCs give bad news by email, they should also give good news by email. For example, email “we really want to discuss a term sheet -- you free to talk tomorrow?” A few times I got cryptic emails from VCs and I assumed it was bad news and so I put off scheduling with them … but it was actually good news. My advice to VCs: get good news into the hands of founders ASAP.

One of the things Sapphire (and some of the other top VC firms) did well is they would email me with an update every 1-2 days (“here is where we are at, here is what we did, here is what we are planning on doing tomorrow”) … those updates put the founder at ease and make running the process much easier.

10. Send Break-up Emails

When a VC doesn’t meet your expectations, send them a break-up email.

During the SafeGraph Series B process, I sent over a dozen break-up emails to VCs letting them know that we were not going to take the step with them. The break-up may have been because (1) they were not the right stage for us; (2) they were not going to add enough value; (3) we thought there was a conflict with one of their other investments; or (4) the VCs missed a deadline and were not moving fast enough.

Many times the break-up email invoked a conversation from the VC (“really sorry we were not moving fast enough. If I can promise to get everything done in two-days, can we get back into the deal?”).

Remember, you are choosing the VC as much as they are choosing you. You might be “married” to this partner for the next ten years -- so you need to choose wisely. No need to waste your time with VCs that are not going to be good fits. This is especially true in today’s more frothy market where you don’t need to collect term sheets just to optimize valuation.

One of the things I am proud of the process we ran at SafeGraph, is that we would have been happy with ALL of the term sheets we got. All of the terms were great and all from fantastic partners. We ended up picking Sapphire but it was a really hard choice (all the firms that gave us term sheets were super high-quality and the individual partners all would have been value-adds).

Assuming you have a quality company, you don’t need to settle for a firm or partner that you don’t think will meet your needs.

If you are a founder in a Series B process, feel free to reach out to me if I can be helpful in any way -- https://twitter.com/auren

What is the acronym 'GLG'?